Carrier Profits, Market Chaos, and Dysfunction

Supply Chain Reactions

A Condensed Update For American Shippers

Issue Date: July 14, 2021

Quote of the Issue:

“There was never a night or a problem that could defeat sunrise or hope.”

– Bernard Williams

Record Carrier Profits Amid Market Chaos and Dysfunction

ShapLight Focus: Ocean carrier profits have already exceeded all of 2020 and are projected to eclipse $100B by the end of 2021, a result that would best the 11 years before COVID combined

- 55% of total Asia to US trade volume touches the port of Yantian, with 10% shipping directly from that massive gateway; it will take months to calculate the total cumulative delay of the work stoppage in Shenzhen

- Blank sailings to the US averaged 80,000 TEUs a week in June as ocean carriers continued to place vessels and containers in their correct circulatory flow; July blanks are expected to diminish to 50,000 TEUs a week, which is still 10% of total capacity

- Drewry estimates that 16% of global capacity is lost due to poor port productivity; American ports are notoriously less productive than those in Asia and Europe

- Global shipping demand is forecasted to increase by 10% in 2021 and another 5% in 2022, while new ship buildings are set to increase capacity by just 4.2% in 2021 and 2.8% in 2022; our days of chronic under-supply are far from over

- Los Angeles and Oakland continue to average more than 15 vessels at anchor or at drift on any given day

- The International Longshore and Warehouse Union (ILWU) contract, which covers the US West Coast, expires in mid-2022

- NVO market share has increased 10%, from 43% to 53%, since 2019 as spot market and premium options now dominate the overall playing field

- Current FAK rates from Asia to US are 350-450% above their 5-year averages, and this does not even include premium surcharges for many carriers

The Biden Administration Targets Ocean Shipping and Railroads

ShapLight Focus: The White House called on the Federal Maritime Commission (FMC) and the Surface Transportation Board (STB) to act against carrier practices that make it onerously expensive for American companies to transport their products

- The US Court of International Trade (CIT) announced that it will halt the liquidation of unliquidated entries subject to 301 tariffs in the wake of the thousands of plaintiffs who filed lawsuits questioning the legality of List 3 and List 4 tariffs on Chinese goods

- Specific to detention and demurrage, President Joe Biden signed an executive order on July 9 that calls for the FMC to “consider further rulemaking to improve detention and demurrage practices and enforcement of related Shipping Act prohibitions”

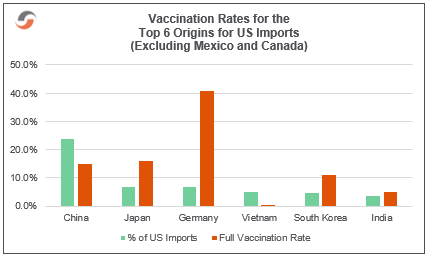

- The US has been generous with global vaccination distribution, but US importers are increasingly worried about the sustainability of their production chains as the Delta variant arrives in countries with low vaccination rates

Airfreight Costs at Lowest Relative Cost to Ocean in History

ShapLight Focus: The cost of airfreight relative to ocean is typically over 1000% and averaged 1200% higher in 2019; with ocean freight skyrocketing, airfreight is only 600% more expensive, a new record for this measure (and despite a 77% increase in air rates since 2019)

- Speaking of rates, YTD airfreight rates for 2021 are 77% higher than 2019, with almost exactly the same chargeable volume; reduced capacity continues to support higher rates

- General Sales Agents (GSAs) now book an impressive 25.3% of all air cargo globally

- International load factors for air cargo hit 65%, which is 13 percentage points higher than historical averages; airlines are certainly doing the most with the capacity present

- eComm currently represents 16% of global airfreight, but experts project that eComm will occupy 33% of air cargo volume by 2025; the value of eComm cargo is projected to be $4.4 trillion

- Global airfreight capacity continues to expand gradually though it is still 10-11% lower than in 2019

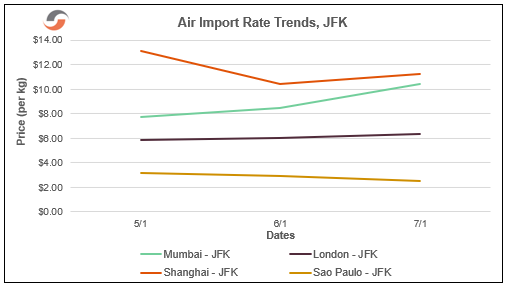

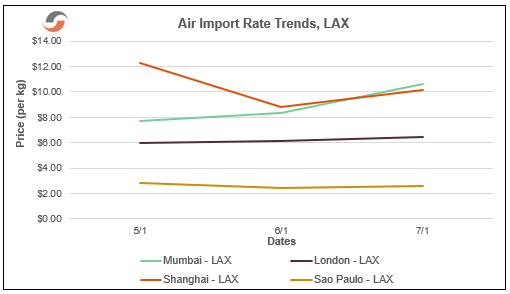

Please note the following three-month airfreight rate trend charts:

Airfreight Costs at Lowest Relative Cost to Ocean in History

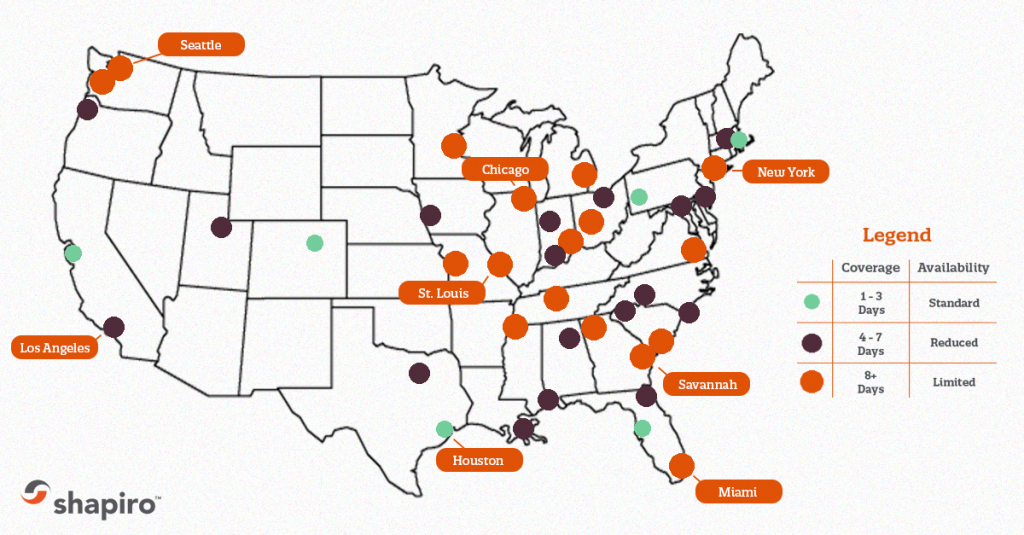

ShapLight Focus: Please see our map of average dwell times at key US ports and rail ramps:

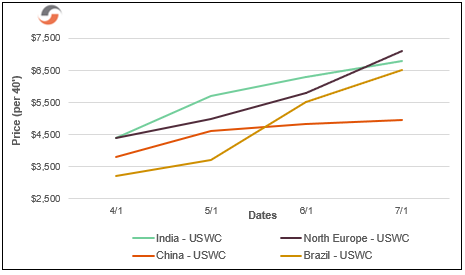

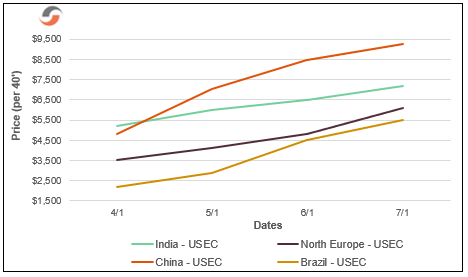

Ocean Freight Rate Trend Charts

Ocean Import FAK Rates to US West Coast (per 40’):

Ocean Import FAK Rates to US East Coast (per 40’):

Our Expert Shapinion

#1: Knock, Knock. Who’s There? Water? Water Who?

Water You Dewing Telling Knock Knock Jokes?

Look, not only is the current market a joke, but it is a joke within a joke within a vicious circle. Suez + Yantian + Blank Sailings + Port Congestion + Detention and Demurrage + Dislocated Containers and Vessels + Skyrocketing Rates … and they all feed the same cycle, again and again. We might as well laugh!

#2: Knock, Knock. Who’s There? Figs. Figs Who?

Figs this US Infrastructure, Please!

Our ports can’t handle mega vessels efficiently, and the overall import volume overwhelms our truckers, our railroads, and our ports while leaving our exporters high and dry. The time has come to improve our roads, bridges, rails, ports, and the underlying transportation technologies. China is outpacing the world when it comes to infrastructure investments; we better wake up!

#3: Knock, Knock. Who’s There? Police. Police Who?

Police Help us with Better Detention and Demurrage Rules, FMC!

In a recent survey, American importers estimated that 15% of their freight budgets were now devoted to demurrage and per diem. This comes at a time when freight rates are 350-450% higher than their five-year averages! That is an “E” on the calculator, y’all!

#4: Knock, Knock. Who’s There? Stopwatch. Stopwatch Who?

Stopwatch You are Doing, Steamship Lines!

We are all so very deeply sorry that your industry struggled with profitability in the decade before COVID, and we too were terrified early in 2020. However, the time has come to focus on fairness, scalability, and a return to collaboration, communication, and partnerships.

When freight rates eclipse $20,000, is it really the best time to be layering in new congestion and inland surcharges? Is it the best time to take a hard line on demurrage? Do you really want to invite regulators and government oversight to our already highly inefficient party?!

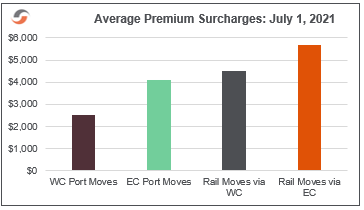

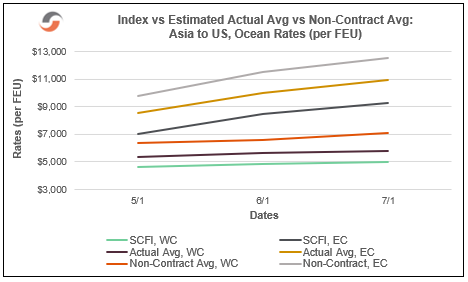

Chart of the Issue:

#5 Knock, Knock. Who’s There? Dozen. Dozen Who?

Dozen Anybody Else See that Smaller Importers are Being Squeezed Out?

Especially for lower value and heavier cargo, the current high costs and long transit times make international sourcing all but impossible. At the same time, the monolithic wealthy big importers can out-bid the smaller guys when supply is so very scarce. While they may not be actually paying

$20,000, Walmart certainly CAN and WILL pay whatever it takes to secure inventory.

#6 Knock, Knock. Who’s There? Razor. Razor Who?

Razor Hands if You Think Today’s Consumer Demand is Loco!

Talk about a vicious circle. With inventory to sales ratios at 20-year lows, importers are desperate to replenish inventories in part because their supply chains are literally broken with huge delays at each link. At the same time, America seems to be in a goods AND services demand frenzy. While it seems like services will become dominant again, the question is when!

#7 Knock, Knock. Who’s There? Ice Cream. Ice Cream Who?

Ice Cream every single day in today’s market!

Exactly. Enough said.

Shap Fact of the Issue:

Gallup reported that the percentage of American adults who consider themselves to be “thriving” has reached nearly 60%, an all-time high since the Gallup first published the index in 2008.

The leadership and staff of Shapiro understand the personal and business anxiety each of you is experiencing. We want nothing but safety today and a return to normalcy tomorrow for you and your families. Please reach out to us if you have any questions—or if we can assist you in any way.